Nonprofit financial statements are essential tools for ensuring accountability, transparency, and effective financial management within nonprofit organizations. Whether you are a board member, financial officer, or simply involved in nonprofit financial oversight, understanding these reports is crucial to maintaining compliance with regulations and ensuring the trust of donors, grantors, and stakeholders.

In this article, we will explore the key components of nonprofit financial statements, how to read and analyze them, and their significance in maintaining a healthy financial structure within your organization.

-

What Are Nonprofit Financial Statements?

Nonprofit financial statements are formal records that outline the financial activities and condition of a nonprofit organization. Unlike for-profit businesses, nonprofits are driven by a mission rather than profit generation, but they must still maintain precise financial records to demonstrate accountability and stewardship of resources.

These financial reports typically include the following main documents:

- Statement of Financial Position (Balance Sheet)

- Statement of Activities (Income Statement)

- Statement of Cash Flows

- Statement of Functional Expenses

Each of these plays a vital role in providing a clear and complete picture of a nonprofit’s financial health.

-

Importance of Nonprofit Financial Statements

Nonprofits rely heavily on donations, grants, and other sources of funding to support their operations. Transparent and accurate financial reporting helps:

- Gain donor trust by demonstrating how funds are allocated.

- Meet regulatory compliance and filing requirements.

- Make informed decisions regarding program expansion or cost management.

- Attract new funding opportunities by showcasing financial responsibility.

Properly maintained financial statements are also critical for IRS reporting and adherence to GAAP (Generally Accepted Accounting Principles), which nonprofits are required to follow.

-

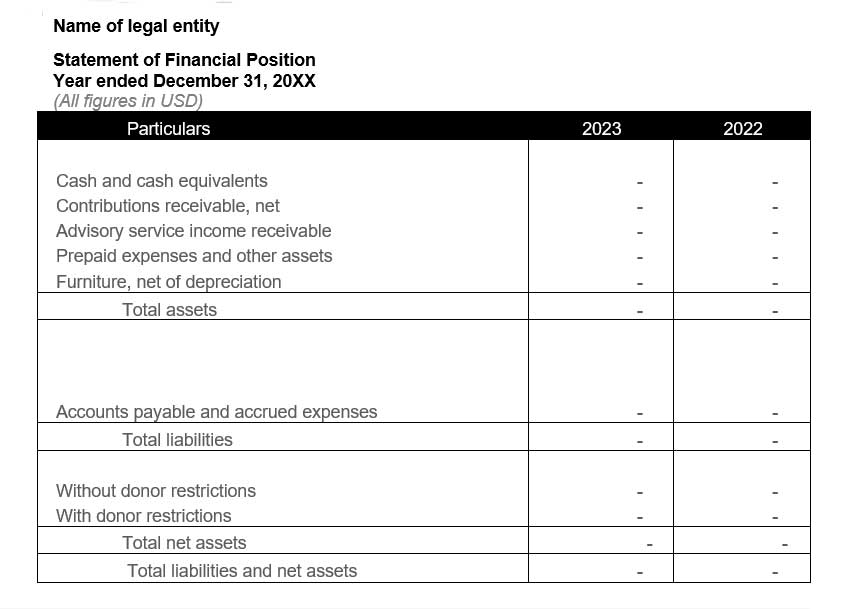

Statement of Financial Position (Balance Sheet)

The Statement of Financial Position, commonly referred to as the balance sheet, outlines an organization’s assets, liabilities, and net assets at a specific point in time. For nonprofits, net assets are categorized as unrestricted, temporarily restricted, and permanently restricted, based on donor stipulations.

Key Elements of a Nonprofit Statement of Financial Position:

- Assets: These include both current assets (e.g., cash, receivables) and non-current assets (e.g., property, equipment).

- Liabilities: Short-term liabilities (e.g., accounts payable) and long-term obligations (e.g., loans).

- Net Assets: Represents the difference between assets and liabilities, classified by restrictions imposed by donors.

Why It Matters:

The Statement of Financial Position provides a snapshot of an organization’s financial standing and its ability to meet short-term obligations and sustain long-term growth.

A specimen format of Statement of Financial Position is shown below.

-

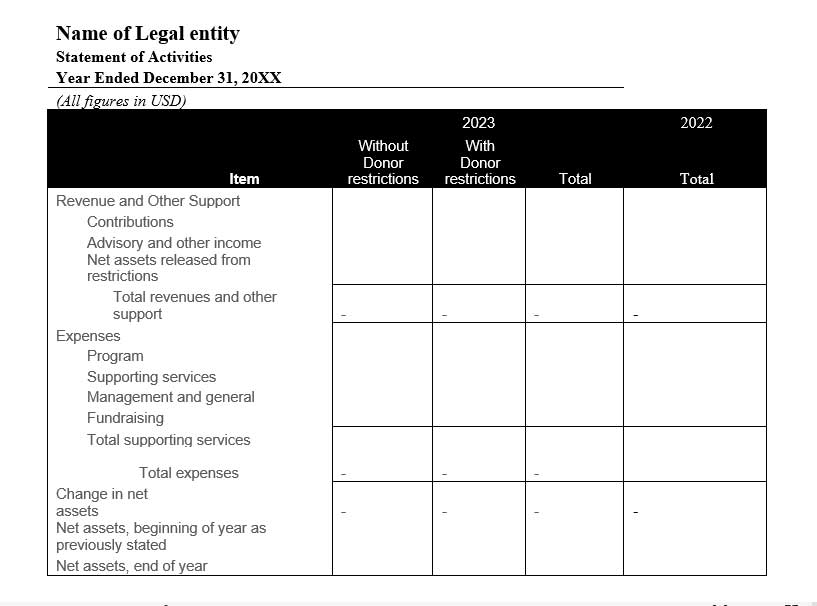

Statement of Activities (Income Statement)

The Statement of Activities details an organization’s revenues and expenses over a reporting period, much like a for-profit company’s income statement. However, nonprofits track changes in net assets rather than profits.

Key Elements of a Nonprofit Income Statement:

- Revenues: These may include contributions, program service revenue, membership fees, and grants.

- Expenses: Divided into program services (expenses directly related to mission work) and supporting services (administrative and fundraising costs).

Why It Matters:

This statement shows how effective the nonprofit is in managing its resources to support its mission. Donors often analyze this document to assess operational efficiency.

A specimen format of Statement of Activities is shown below.

-

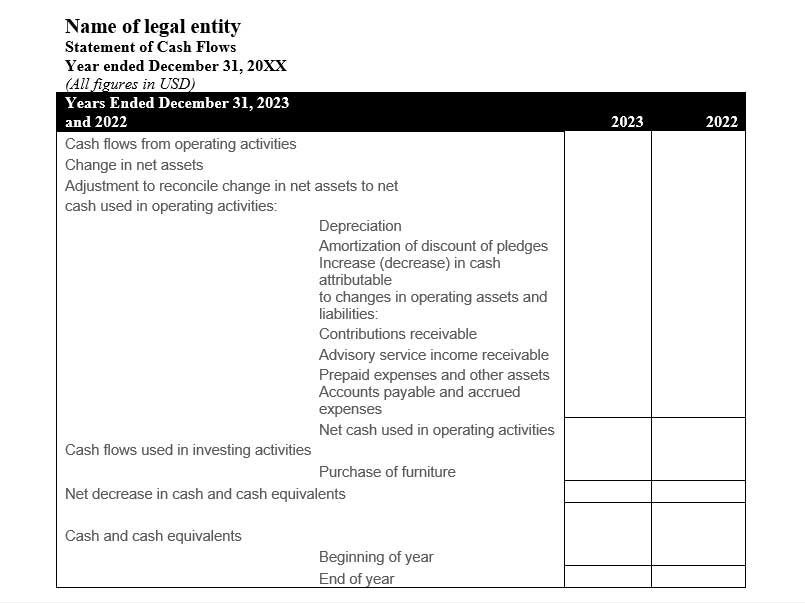

Statement of Cash Flows

The Statement of Cash Flows tracks the movement of cash in and out of the organization, highlighting operational, investing, and financing activities. It is crucial for assessing the liquidity and overall financial flexibility of a nonprofit.

Key Elements of a Nonprofit Cash Flow Statement:

- Operating Activities: Daily operations, including incoming donations and outgoing payments.

- Investing Activities: Purchases or sales of long-term assets like equipment.

- Financing Activities: Funds related to loans, grants, or endowments.

Why It Matters:

This statement is vital for assessing cash availability and ensuring the nonprofit can continue funding its programs without liquidity issues.

A specimen format of Statement of Cash Flows is shown below.

-

Statement of Functional Expenses

The Statement of Functional Expenses is unique to nonprofit organizations and outlines how expenses are allocated between program services, management, and fundraising. This report is particularly useful for donors who want to see how efficiently the organization uses its resources to further its mission.

Why It Matters:

Breaking down expenses by function helps nonprofits demonstrate their commitment to using funds efficiently, which is essential for maintaining donor trust and fulfilling IRS requirements for public disclosure.

A specimen format of Statement of Functional Expenses is shown below.

-

The Role of Audits in Nonprofit Financial Statements

Regular audits are a key part of ensuring the accuracy and reliability of nonprofit financial statements. Independent audits help verify that the financial statements present a fair and accurate view of the organization’s financial position.

Auditors check for:

- Compliance with GAAP.

- Proper internal controls.

- Correct classification of revenues and expenses.

- Any incidence of fraudulent activities.

- Going concern assessment.

Most importantly, a clean audit report can build confidence with donors, grantors, and governmental agencies, showing that the organization follows best practices in financial management.

-

Nonprofit Accounting Standards and Compliance

Nonprofits must adhere to accounting standards such as GAAP and, in some cases, FASB (Financial Accounting Standards Board) guidelines. These standards ensure uniformity in reporting and transparency for stakeholders.

-

IRS Guidelines: Form 990 Requirements

Non-profits must file IRS Form 990 annually, and financial statements are a key part of this submission. Key IRS requirements:

- Statement of Functional Expenses is crucial for showing how much is spent on program services versus administrative and fundraising costs.

- Public Support Test: Non-profits must prove they receive a substantial portion of support from the public. This requires careful categorization of revenue streams.

- Disclosure of Executive Compensation: Any salaries for top officers must be transparent.

Failure to comply with these standards can result in penalties and loss of tax-exempt status, making compliance a priority for nonprofit financial teams.

-

10. How to Improve Nonprofit Financial Reporting

Effective nonprofit financial reporting begins with:

- Accurate bookkeeping: Ensuring that all transactions are recorded properly.

- Regular reviews: Holding financial review sessions with the board or finance committee.

- Using accounting software: Implementing nonprofit-specific accounting software to track restricted and unrestricted funds.

- Engaging with professional accountants: Working with CPAs or financial consultants who specialize in nonprofit organizations can ensure that reporting aligns with regulations and best practices.

- Best Practices for Nonprofit Financial Management

To maintain financial health, nonprofits should adopt the following best practices:

- Diversify revenue streams: Rely on various income sources, such as donations, grants, and program fees.

- Maintain a reserve fund: Set aside funds to cover unexpected expenses or revenue shortfalls.

- Budgeting and forecasting: Develop accurate budgets and financial forecasts to plan for the future.

- Board involvement: Engage the board of directors in financial oversight to ensure checks and balances.

-

Conclusion – Nonprofit Financial Statements

Nonprofit financial statements are critical tools for ensuring transparency, accountability, and informed decision-making. From the Statement of Financial Position to the Statement of Functional Expenses, each report serves a unique purpose in evaluating and managing a nonprofit’s financial health. By understanding these financial statements, nonprofit leaders can make strategic decisions that support the organization’s mission and long-term sustainability.

FAQs – Nonprofit Financial Statements

Q1: What is the most important financial statement for nonprofits?

All four main statements (Balance Sheet, Income Statement, Cash Flow Statement, and Functional Expenses) are equally important as they provide different insights into the organization’s financial status.

Q2: What is the difference between a for-profit and a nonprofit financial statement?

The main difference is that nonprofits focus on the mission and net assets rather than profit, and they must classify funds based on donor restrictions.

Q3: How often should nonprofits prepare financial statements?

Nonprofits should prepare these reports at least annually for their stakeholders, with internal reviews conducted quarterly or monthly.

Q4: What are unrestricted, temporarily restricted, and permanently restricted funds?

These terms refer to how donors intend their contributions to be used. Unrestricted can be used for any purpose, temporarily restricted for specific purposes, and permanently restricted for endowments.

Q5: Do nonprofits need to follow GAAP?

Yes, nonprofit organizations must adhere to GAAP to ensure their financial statements meet regulatory standards and offer transparency.

Q6: Why is the Statement of Functional Expenses unique to nonprofits?

This statement breaks down expenses by function, highlighting how much money is spent on program services, management, and fundraising, offering detailed insights into a nonprofit’s operational efficiency.

For detailed guidelines on nonprofit accounting standards, visit FASB’s website

To Read More Blogs on FAQS on Global Nonprofits by B.D.Chatterjee, Click Here..